USDA loan does have a long history and has been referred to by other names over the years but today it’s one of the least utilized home loan programs in today’s market when it really shouldn’t be. The USDA origins can be traced back to 1946. Then, the Farmers Home Administration, or FmHA, was established to replace the Farm Security Administration.

USDA loan does have a long history and has been referred to by other names over the years but today it’s one of the least utilized home loan programs in today’s market when it really shouldn’t be. The USDA origins can be traced back to 1946. Then, the Farmers Home Administration, or FmHA, was established to replace the Farm Security Administration.

In 1990, the Rural Development Administration was formed under the auspices of the United States Department of Agriculture. The RDA’s mission is to provide assistance to those in rural areas with business loans, grants and community development programs. It is here where the USDA home loan is administered.

The USDA loan program is one of three government-backed mortgage loans, the other two loans in this category are the VA and HUD FHA mortgages. With the USDA loan, there is no down payment requirement for this special program making it easier for those who live in rural areas to buy and finance a home.

The USDA home loan guarantee is funded through what is known as the Guarantee Fee, which is 1.0% of the purchase price of the home and is sometimes referred to as the “upfront” fee because it is settled at the closing table and rolled into the loan amount. It is not paid out of pocket. There is an additional fee charged once per year called, appropriately, the Annual Fee.

This amount today is 0.35% of the outstanding loan balance and is paid in monthly installments along with the principal and interest payment, taxes and insurance. Think of this as something similar to PMI. These two premiums are paid for by the borrower with the lender as the beneficiary and apply to USDA loans used for both purchase and refinance transactions.

Many consumers aren’t aware of this program and instead resort to a conventional loan. However, conventional mortgages will require a down payment of 3%-5% causing the borrowers to come to the closing table with more money. This may be difficult for many first-time buyers.

What exactly is rural according to the USDA? The USDA has already declared certain regions as rural and makes adjustments to these zones once every 10 years after the most recent census has been completed. To find out if an area is in an approved zone the loan officer will visit the USDA website and type in the property address. If the property is in an approved zone the USDA will accept the property. If not, the buyers must find a property that is located in an approved area or otherwise use another loan program like FHA, etc.

Because the adjustments to these areas take place once per decade areas can be included in an approved area that looks nothing like rural property. For example, as property values increase the closer you are to urban areas, buyers seek to finance a home further out for a better deal. Developers recognize these trends and develop new subdivisions that soon readily populate an area. Schools and shopping can soon follow. Yet a property can still be in an approved USDA zone even though there houses all around.

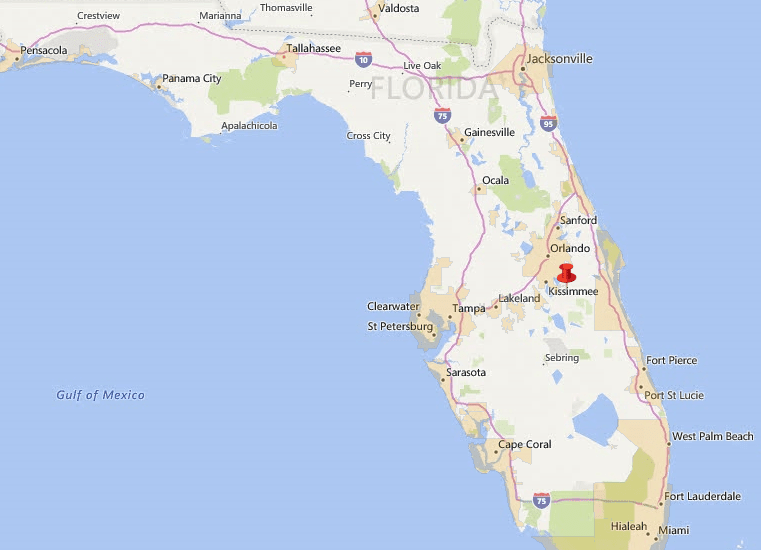

In such an instance, a property can be in an approved zone today due to the age of the most recent census but next year is out of an approved zone due to the newly designated areas defined by the USDA. You won’t find approved areas in populated locations like Orlando, Jacksonville, Tampa, Miami, but you might very well be surprised to discover many of the outer suburbs are approved. The map below shows the general USDA approved locations, pay attention to the darker areas. These are locations not eligible. Buyers can learn more about USDA loans by calling ph: 800-743-7556 or just submit the Quick Form on this page.