Atlanta VA Home Loans offer eligible home buyers many advantages. 100% financing, no PMI, low fixed interest rates to name a few. In the post below, we will take a look at the VA loan advantages for homebuyers in 2024.

Atlanta VA Home Loans offer eligible home buyers many advantages. 100% financing, no PMI, low fixed interest rates to name a few. In the post below, we will take a look at the VA loan advantages for homebuyers in 2024.

Georgia home buyers that have questions can contact VA Mortgage Hub at Ph: 800-743-7556 or just submit the info request form on this screen for a quick call back. We have local loan specialists standing by 7 days a week to assist you.

100% Financing VA Atlanta:

$0 down payment to qualify for a VA Home Mortgage Loan for up to $4,000,000 in Georgia. 100% home loan options are getting harder to find. The is great for Vets in Atlanta and other higher costs areas in GA. Also, if the seller agrees to pay the closing costs, you may be able to purchase the home with no out of pocket cost. VA will allow the home seller to pay the buyers VA allowable closing costs. The loan and sales contract can be set up so that the VA loan covers 100% of the selling price and the seller covers the closing cost.

Qualifying for a VA Mortgage Loan:

The VA offers flexible qualifying standards on their veteran loans. Even if you have experienced some financial difficulties in the past that may have caused your scores to be low, you still may qualify for a VA mortgage loan. This can be a tremendous saving compared to the cost of conventional or FHA loans when the borrower’s credit scores are low. Note, most lenders require a 600 credit score to be approved.

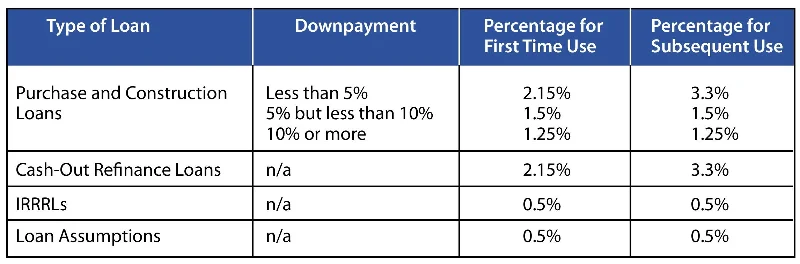

Georgia VA Funding Fee Chart:

The Veterans Administration assesses a funding fee for all VA loans between .5% and 3.6% of the loan amount. The fee is added to the amount of the loan to be paid over the life of your VA home loan. The VA Funding Fee replaces the much higher-priced mortgage insurance required when you get a conventional home loan. No monthly mortgage insurance ( PMI) is a great advantage to VA loans. Also, If you are a Disabled Veteran, you may qualify to get the fee waived completely. Please see the 2024 funding fee chart below.

VA Loans Can Be Refinanced:

VA mortgage loans have built-in features allowing a loan to be refinanced to a lower interest rate without all the criteria normally associated with a conventional loan. This is called an IRRRL or Interest Rate Reduction Loan; the veteran can secure a lower interest rate without any credit checks, appraisal, and income or asset verification. All the costs can be can roll in the transaction, so there are no out-of-pocket costs. Homeowners can learn more about the VA refinance here. VA also permits up to 100% cash out refinance for homeowners that have equity and would like to cash out for home remodel or debt consolation.

VA Jumbo Loans:

Many Vets are unaware that VA permits 100% financing for high-cost loans under the special VA Jumbo program. The VA Jumbo program will require payment reserves, and of course normal debt to income requirements do apply. VA Jumbo loans are a great option for veterans who are looking to purchase or refinance a higher priced home. With loan amounts up to $4 million and 100% financing available, this program allows eligible veterans to secure their dream home without having to worry about a down payment.

One of the key benefits of VA Jumbo loans is that they do not require private mortgage insurance (PMI) just like normal VA loans. This means that veterans can save thousands of dollars over the life of their loan compared to other conventional jumbo loans that typically require PMI when putting less than 20% down.

Interested home buyers can learn more by calling the number listed above, or just submit the Info Request Form on this page.

Serving all of metro Atlanta: Fulton, DeKalb, Gwinnett, Cobb, Clayton, Coweta, Douglas, Fayette, and Henry County. Alpharetta, Ansley Park, Atlanta, Atlantic Station, Buckhead, Cabbagetown, Candler Park, Castleberry Hill, Chattahoochee Hills, College Park, Johns Creek, Little Five Points, Midtown, Milton, Mountain Park, Old Fourth Ward, Palmetto, Poncey-Highland, Roswell, Sandy Springs, Union City,